The Netherlands – Holland Hydrogen I, an electrolysis project near the Port of Rotterdam, has earned Shell’s final investment decision (FID), kicking off the development of a large hydrogen sector in the Netherlands.

ICIS explores how Shell made this financial decision, why the Netherlands is a hotspot for hydrogen project announcements, and if other project developers may mimic Shell’s success.

Dutch decarbonization efforts rely heavily on hydrogen. Shell announced FID on a 200MW electrolyzer project near Rotterdam in July 2022. This is Shell’s first large-scale renewable hydrogen plant and the Netherlands’ first commercial-scale hydrogen project.

The Dutch government promotes hydrogen supply projects financially and politically since hydrogen is key to its future energy mix. The Dutch government is committed to attaining net-zero emissions by 2050 and wants to reduce the country’s dependency on fossil fuels, especially since the Groningen field, the country’s largest gas reserve, will be decommissioned in 2023.

Next year’s Groningen gas production will be capped to 2.8 bcm (between October 2022-30 September 2023). 2.8 bcm accounts for 7% of yearly Dutch gas usage. 2014 production topped 50bcm.

Dutch heavy industries import a lot of Russian oil and gas. In 2021, 35% of Dutch oil imports were from Russia, and Rotterdam refineries were adapted to produce diesel from Russian crude. Reduced feedstock availability pressures Dutch refineries.

After Russia’s invasion of Ukraine, local gas output declined and supply chain interruptions drew the Netherlands’ attention to renewable energy and low-carbon hydrogen.

The Dutch government will invest €750 million on a national hydrogen pipeline network between 2022 and 2031. The coalition administration wants to develop 3–4 GW of electrolysis capacity by 2030, under the 2020 Hydrogen Strategy.

The Netherlands’ electrolyzer capacity goal is less than half of Germany’s, although Dutch subsidies help project developers more. The Netherlands’ low-carbon hydrogen demand is estimated to vary from 2.8 TWh/year to 12 TWh/year. The government expects these programs to attract projects and help meet those demands.

Due to its closeness to North Sea offshore wind farms and natural gas pipelines, the Netherlands is well positioned for a renewable or low-carbon hydrogen economy. Rotterdam is Europe’s largest container harbor and industrial centre, and a source of hydrogen demand. Dutch salt caves and depleted natural gas supplies could store hydrogen.

EHB development plans are also ongoing. The EHB will use the Dutch L-gas (low calorific gas) network to link industrial clusters across the country. The Netherlands has announced more than 50 hydrogen projects. These initiatives vary in scope and commercial viability.

Shell hydrogen FID

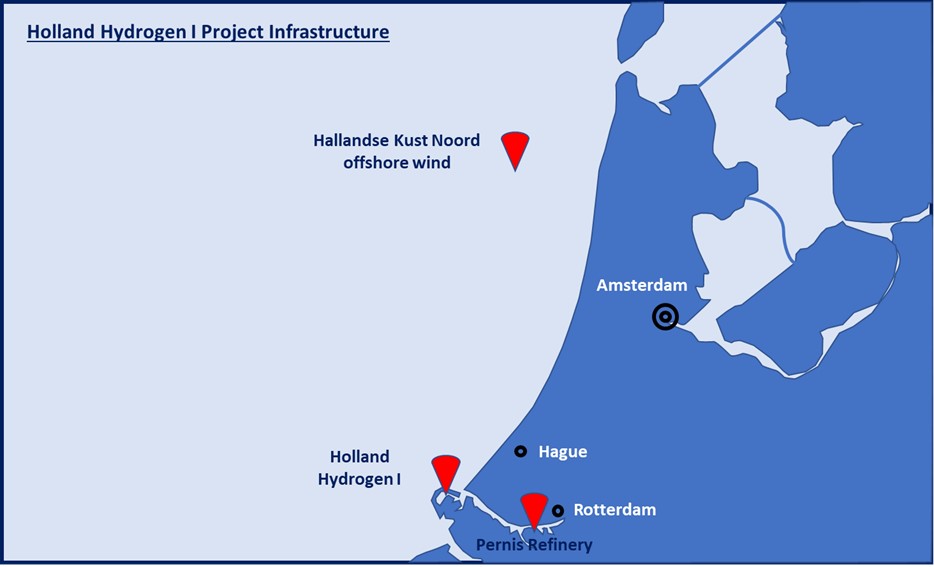

Hydrogen Holland Shell anticipates I production in 2025. If completed on time, it would be Europe’s largest renewable hydrogen plant, producing 60t/day from a 200MW alkaline electrolyzer. Hallandse Kust Noord will supply most of the project’s energy.

Shell and Eneco’s CrossWind collaboration is building the 2024 wind farm. If the grid electricity meets the requirements for creating renewable hydrogen, the electrolysis plant will use grid backup power to deal with the intermittent supply.

Holland Hydrogen I’s hydrogen will be sent to Shell’s Pernis refinery, Holland’s second-largest, to decarbonize it. Without plans to sell hydrogen, the refinery will use all of Holland Hydrogen I’s output. Therefore, Shell won’t need on external demand or market pricing to succeed.

Shell has also built a hydrogen fueling station for 20 Qbuzz hydrogen buses in Groningen, Netherlands, gaining experience with smaller-scale hydrogen distribution. Shell provides green-certified hydrogen at the 2021 station until it can produce its own renewable hydrogen. Shell plans to market low-carbon hydrogen from the NortH2 and H-Vision projects in the Netherlands, which are undergoing feasibility assessments.

Shell took FID on Holland Hydrogen I despite not knowing how to tax hydrogen due to its technical competence, financial clout, and supply chain requirement. Shell’s global program will be modeled after this one.

Will more projects follow Holland Hydrogen I?

ICIS has identified 15 new hydrogen projects in the Netherlands, 11 of which are undergoing feasibility studies and 4 are in the concept stage. If all 15 were online by 2030, they would meet the Dutch government’s electrolyzer capacity goals.

According to an analysis of company statements, by 2030 Shell will have the most electrolyzer capacity in the Netherlands, followed by Gasunie, Equinor, and RWE. Many project participants with financial and technical resources can support large-scale projects. Numerous large firms are determined to complete projects despite negative economics and have investor support for energy transition initiatives.

Staggering hydrogen initiatives reduces risk. ICIS says projects might cost over €100 billion by 2031. Businesses can learn from small operations before growing to larger ones.

Only H2-Fifty, Uniper-Maasvlakte, and HyNetherlands have November 2022 FID dates. This doesn’t guarantee that these projects will move forward, but it shows that many are hesitant to set clear public FID timelines due of planning constraints.

The Netherlands has high hopes for a big hydrogen sector. The government has set lofty targets and provided funds to achieve them.

Shell’s FID on Holland Hydrogen I is a landmark for the Dutch hydrogen industry. Shell may be able to apply this initiative’s lessons to strengthen its other hydrogen-related efforts and gain participants’ trust. There are several companies with the technical know-how, project expertise, and financial strength to build more projects in the Netherlands.

Most of these projects, unlike Holland Hydrogen I, will need hydrogen offtakers. Without a traded market for renewable or low-carbon hydrogen, projects may have trouble finishing. To attract considerable capital investment from stakeholders, more policy support and commercial approaches that decrease project risk are needed.